Investing

Tax-Free Savings Account

")

Apply online to open an account in minutes.

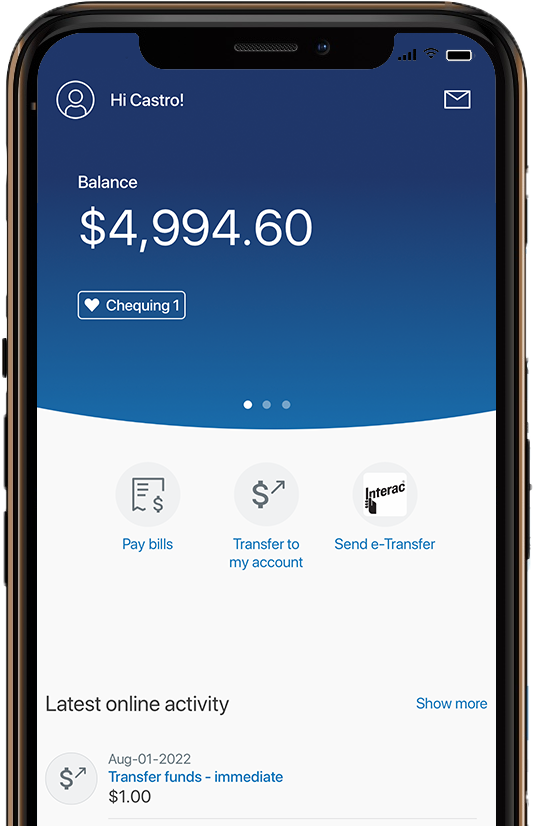

Log in to add a product.

Download the app and sign in!

Welcome to client centered banking and award-winning service, products and total transparency that truly puts the good in banking.

Stay in touch. Be the first to know about news, promotions and announcements. Signup Now!